Many American expats dread the need to open a local bank account when they move to France. They’ve heard the rumors on how difficult it can be and how no local bank will do business with Americans.

While it is difficult for Americans to open a bank account in France, it’s certainly not impossible. Many large and international banks are used to doing business with Americans and regularly accept them as clients. The French bankers may grumble more than usual at the extra paperwork, but opening an account is one of the smaller hurdles to cross when moving to France.

Disclosure: Some links in this article may be affiliate links. If you choose to use them, we may earn a commission at no additional cost to you. We only recommend services we believe are genuinely useful.

Do Americans actually need a French bank account?

Yes, opening a French bank account is an essential step when settling in France. Many services require payment by bank transfer, such as rent, utilities, subscriptions, gym memberships, and car purchases. France has no consumer credit rating, so credit worthiness is often based on having an established history with your local bank.

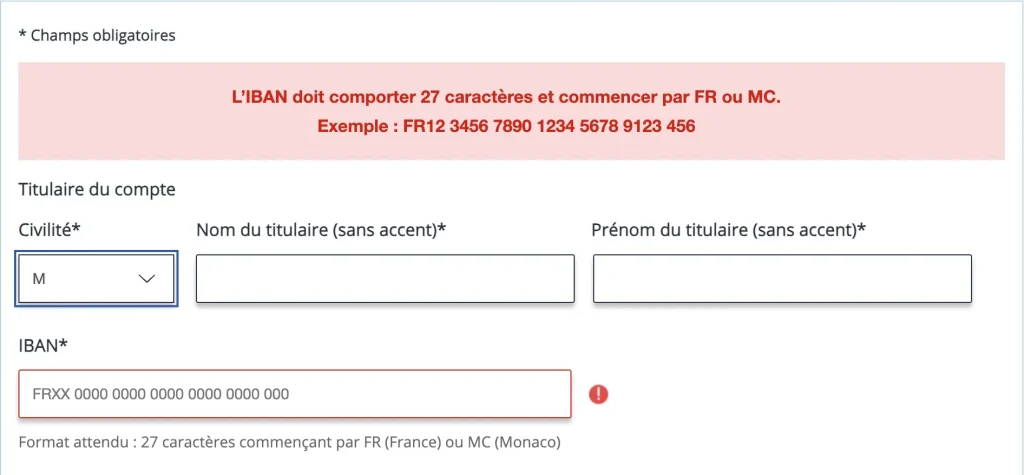

While most payments can be made with any European bank account, thanks to the EU’s regulations on IBAN discrimination, there is one crucial service that requires a French bank account: public healthcare.

In order to apply for the Carte Vitale and receive reimbursements from CPAM, a French account with an IBAN beginning in FR (or MC if you live in Monaco) is a required step.

This is why an account with Wise, an extremely popular choice among expats, is insufficient for handling all French banking needs. The Belgian IBAN currently used for Euro accounts at Wise is sadly not accepted for the Carte Vitale (we tried).

Types of bank accounts in France

Compte Courant – Current Account

Essentially a checking account, the current account is the standard option you’ll want to open. It allows for deposits and withdrawals, usually comes with an ATM card, and can be used for both paying things like rent or utilities and receiving reimbursements from CPAM.

Compte Épargne – Savings Account

French savings accounts can be quite complex, with many different options available. Some options, like the regulated Livret A and LDDS, offer (French) tax-free interest payments. Others, like the Compte sur Livret, are taxable and unregulated.

For Americans, French savings accounts are often unavailable or impractical due to FATCA reporting requirements and unfavorable US tax treatment.

Our recommendation would be to keep savings in a US-based high-yield savings account or multi-currency account.

Documents required to open a French bank account

As with all administrative tasks in France, opening a bank account in France requires extensive proof and documentation. The details vary from bank to bank, but a passport, residency permit, and proof of address, such as a utility bill, are typically required by most banks.

We opened an account with Crédit Agricole two months after arriving, once we found an apartment and had the required proof of address. To open a joint compte courant, we were asked to provide:

- Passports

- Valid visas (inside our passports)

- Proof of address documents (we used electric and cellphone bills, one for each of us)

- Our last three years of US tax returns

- Three months of bank statements (US bank)

- Marriage certificate (only for joint accounts)

None of our US documents had to be translated and the bank manager we worked with spoke fluent English. He was also quite familiar with American tax documents and had clearly done this many times before.

We also didn’t need a CDI or any French income to open the account. Our US tax returns were sufficient to prove the origin of our funds.

FATCA and why Americans get rejected

FATCA, or the Foreign Account Tax Compliance Act, is the US law responsible for Americans having so much trouble opening financial accounts abroad.

FATCA requires all foreign financial institutions to report details on accounts held by any US citizen. Noncompliance can come with huge penalties for the financial institutions.

Because the penalties are so high, many banks find it less risky to simply not work with any Americans. Generally, only the largest international banks have the resources to comply with FATCA and are willing to take on Americans as clients.

Traditional French banks that sometimes accept Americans

Not every branch is guaranteed to accept Americans, even if the bank brand is known to. However, many expats have success with the large, international banks:

- Crédit Agricole (our old bank)

- BNP Paribas

- Société Générale

- LCL

- N26 (our new bank, online-only)

Opening an account will generally take several weeks. You’ll most likely need to call or show up in person to schedule a rendez-vous with a bank manager, where you’ll submit your dossier with all the required paperwork.

Online banks and fintech options

App-based banks with no physical locations are a growing option, both in the US and abroad. Because there’s no branch to submit paperwork to, the account opening process can be easier and more efficient.

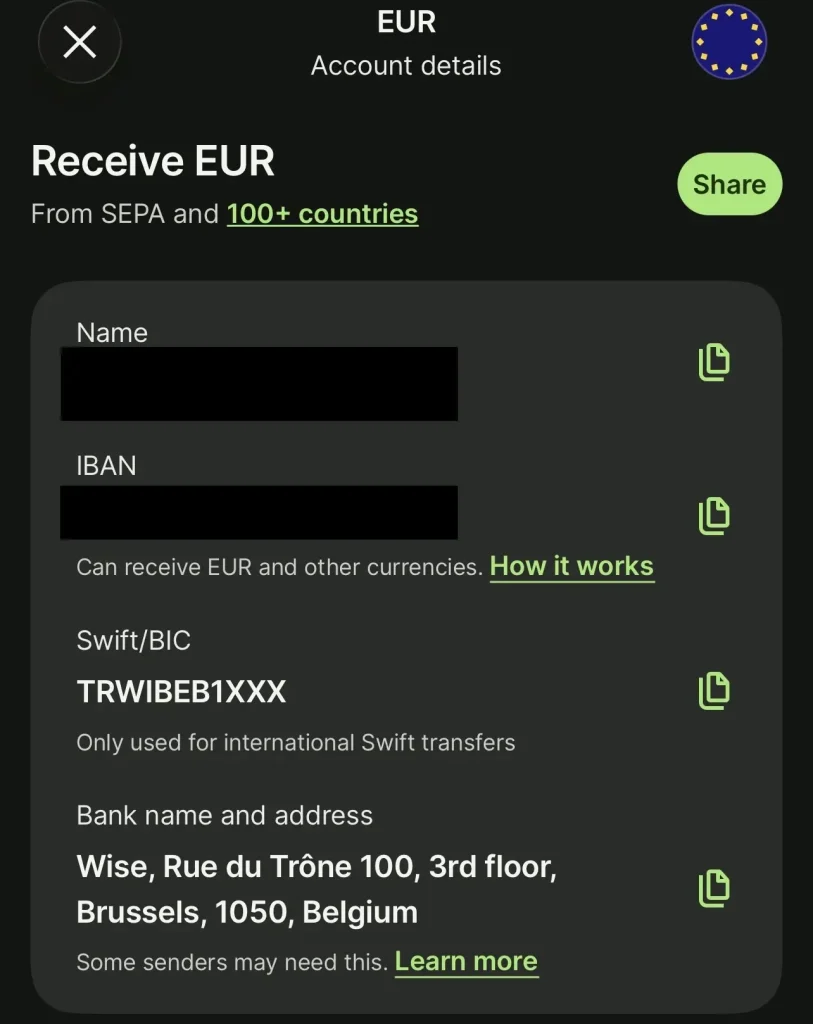

Wise

Wise offers multiple currency accounts, making it easy to deposit Dollars, convert to Euros, and pay bills, transfer to a local bank, or withdraw with a debit card. Better yet, they pay a competitive interest rate on the currencies held.

Wise’s Euro account includes an IBAN which can be used to make SEPA and Swift transfers, an essential way to pay for services like rent and utilities that don’t accept credit card.

Anywhere in France that asks for a RIB, relevé d’identité bancaire, can accept the IBAN from your Wise account. However, because the IBAN is Belgian, it cannot be used with CPAM when signing up for the Carte Vitale. In our experience, this is the only reason a local bank is required, and Wise can’t suffice for everything.

N26

N26 is an online-only bank in France known to accept Americans. Unlike most traditional French banks, which charge €10-€15 per month in account fees, N26 offers a Standard account with zero fees.

Because of the zero fees, we switched to N26 after using Crédit Agricole for our first year, saving €12/month.

If you won’t be needing to frequently withdraw cash at an ATM (or using your Schwab Investor Checking account for the reimbursements), this can be a great way to save on monthly fees.

Managing money between the US and France

Daily Spending – Credit Card

Most vendors in France accept contactless credit card payments, and it’s quite rare to need to pay in cash. For all of our daily purchases, we use a US credit card with no foreign transaction fees. It’s much easier to sign up from the US, so make sure to bring several with you when moving.

Currently, we’re using the Apple Card for the 2% cash back on contactless Apple Pay, no foreign transaction fees, and no annual fee. The cash back is more than enough to offset any conversion rate losses charged by the Visa or Mastercard network.

Monthly Currency Conversion – Wise

For the monthly expenses that can’t be paid with card, we use Wise. Each month, we transfer enough Dollars from our investment accounts to Wise and convert them to Euros. We then pay our bills from our Wise account. For us, that’s rent, utilities, gym membership, and mutuelle insurance. The fees for the conversion usually fall between 0.25%-0.3%.

Large Currency Conversion – IBKR

For very large, occasional currency conversions between the US and France, we use Interactive Brokers. They charge a flat $2 fee, making it more advantageous than Wise for conversions over $800.

However, IBKR discourages using its platform only for currency conversion. Because of this, we only use the currency conversion for large transfers, like buying a car or making a down payment.

FAQs

Can a US citizen open a bank account in France?

Yes, American citizens are free to open bank accounts in France. Due to FATCA, some smaller French banks may not accept Americans as clients. There are, however, plenty of larger banks that will happily take on US citizens.

Can I open a French bank account without residency?

This one is much trickier. Without proof of a local address, most French banks will not open an account. As a non-resident, the best course of action would be to use an online bank such as N26 or open a multi-currency account with Wise.

An online bank is sufficient to establish yourself in France. Once you’ve settled and have proof of address, opening a local French bank account becomes much easier.

Is Wise considered a French bank account?

No, Wise’s Euro account is based in Belgium, and there is currently no option to receive a French IBAN. The Belgian IBAN is sufficient for most purchases, but receiving reimbursements from the public healthcare system requires a French IBAN.

How long does it take to open a French bank account?

It can take 1-2 weeks to open an account at a French bank after submitting all the required documents. Receiving the debit card in the mail may take another few weeks.

Conclusion

Opening a bank account in France as an American is manageable with the right expectations and tools. Many larger banks accept US clients regularly.

If you’re still in the planning stages of your move to France, open a multi-currency account with a European IBAN to make payments in France easy. Then take your time with the local bank account.

Questions? Comments? We’d love to hear from you in the comment section, or feel free to write us directly.

🥖 🧀 🍷

Subscribe to our Newsletter and never miss a post!

Leave a Reply